Sustainability or ESG (Environmental, Social and Governance) reporting has been on the rise for several years[1]. This trend is only accelerating as we speak due to a number of factors, including the following:

One reason is that the urgency of global societal challenges is becoming more visible and better understood. For instance, on February 28, 2022, the Intergovernmental Panel on Climate Change, the UN body of the world’s leading climate experts, reported its “bleakest warning yet”[2] on the impacts of climate breakdown and called once again for urgent action to deal with the increasing risks (IPCC).

At the same time, the impacts of those challenges are starting to hit closer to home. Just look at the summer heatwaves in Europe which seem to become a recurring event. Or open any newspaper to read about yet another flood causing the loss of multiple lives. And issues like water scarcity are no longer a curiosity in Western Europe, but a true concern to be reckoned with. Overall, the tone of the messages is becoming increasingly forceful, pressing us to be aware, alert, and ready. There’s a greater need to understand what is happening and why, and to know how to prepare for and prevent – or at least mitigate – the consequences.

This awareness also encourages people to become increasingly more vocal about what they expect in terms of sustainability. At Sustenuto, for example, we note that our customers cite employer branding as an important reason to work on sustainable development.

And even the COVID-19 pandemic has helped push sustainability to the top of the agenda of governments and organisations worldwide for a number of reasons. For example, it revealed weak spots in supply chains and the cost of optimising efficiency at the expense of resilience. Resilience which is, when it comes to sustainability, absolutely key.

All of this obviously did not escape the attention of Europe either. And so, EU regulation is also focussing more and more on sustainability. In fact, the EU’s growth strategy, i.e. the EU Green Deal, incorporates ambitious sustainability rules and goals and uses tools such as the EU Taxonomy to encourage funds to flow to the development of a more sustainable society. In addition, mandatory sustainability reporting, as per the Non-Financial Reporting Directive (NFRD), is another tool in the EU’s toolbox to support this transition. More on that below.

Finally, the interest of investors and other financial market participants in ESG matters is spiking. Partly because of mandatory requirements imposed upon these parties (see for example the Sustainable Finance Disclosure Regulation (SFDR) which imposes certain ESG-related disclosure requirements). Partly because the links between sustainability related matters, which are considered “non-financial”, and their consequences, which are oftentimes financial in nature, are starting to become more prominent and relevant. Hence, investors want and need to understand better and, in more detail, how (potential) investee companies are doing on the sustainability front.

Obtaining these insights, disclosing this type of information to employees, customers, and investors, and thinking about the role of your organisation from a sustainability point of view requires data. The right data. Data that is complete, reliable, comparable, and accessible.

And this is where voluntary and mandatory sustainability reporting frameworks come into play. At the minimum, these frameworks attempt to provide guidance as to what data is required and how the data should be considered[3].

And so, more and more companies embark on the journey of sustainability reporting. Making use of a variety of reporting frameworks and tools. Some tools are more topic oriented, such as TCFD (Task Force on Climate Related Financial Disclosures) focussing on climate change. Others are more sector oriented, such as the United Nations Principles for Responsible Investment (UNPRI). And then there are frameworks such as the GRI Standards that can be used as a more comprehensive framework altogether.

EU regulations for non-financial companies

In parallel to voluntary sustainability and ESG frameworks, Europe also tirelessly works on sustainability reporting and disclosure regulations. The pillars of EU’s sustainable reporting for non-financial companies are the Non-Financial Reporting Directive (NFRD) and the EU Taxonomy.

The NFRD

In summary, the NFRD, which is currently in effect, imposes mandatory disclosure obligations relating to ESG matters on EU-listed large entities (or parent companies of large groups) with more than 500 employees[4].

In 2021, the European Commission fitness-checked the NFRD and concluded that more information and more reliable and detailed information from a larger group of companies is needed. This resulted in a proposal by the European Commission to amend and replace the NFRD. This proposal, which was issued on April 21, 2021, is called the Corporate Sustainability Reporting Directive (CSRD). On June 21 of this year, the European Parliament and the Council reached a provisional political agreement on the proposal (cf. New rules on corporate sustainability reporting).

The CSRD

In a nutshell, the political agreement on the proposed CSRD includes the following features:

The scope of companies subject to mandatory sustainability reporting is expanded to all large companies (or parent companies of large groups) and to certain listed SMEs[5]. Certain non-European companies generating a net turnover of EUR150 million in the EU will also be obliged to publish certain sustainability related information.

More information is required, including on the company’s plans to ensure that the business model and strategy are compatible with the transition to a low-carbon society and with the limitation of global warming to 1,5°C in line with the Paris Agreement.

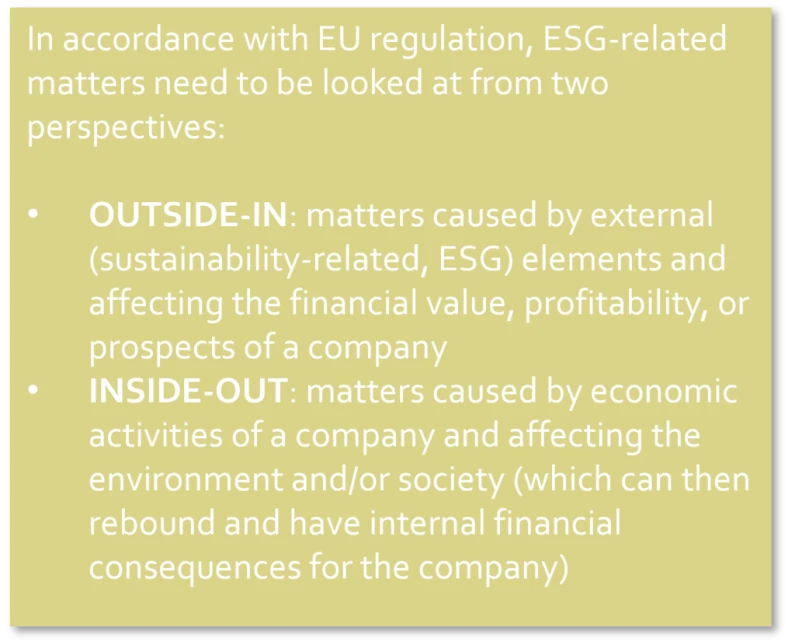

Sustainability related matters also need to be looked at from an inside-out and an outside-in perspective (double materiality, cf. box above).

More detail is specified on what information must be reported based on mandatory reporting standards. A lighter version will be available for SMEs.

Greater assurance of information is required.

Better alignment with other sustainability reporting requirements is ensured.

Reporting is required to be done digitally in an electronic format.

More reliability of the information is allowed for.

The CSRD as it currently stands provides for a deferred application in different stages[6].

Before the CSRD comes into effect, the provisional agreement first needs to go through a legal-linguistic review and translations and must then be formally adopted by the Council and the European Parliament. This process is expected to take up to two to three months. Finally, the CSRD will also need to be transposed into national law.

The EU Taxonomy

The EU Taxonomy is first and foremost a classification tool that helps to identify environmentally sustainable activities. Through a reference to the NFRD, the EU Taxonomy also imposes certain disclosure obligations relating to environmentally sustainable activities. First disclosures under the EU Taxonomy have now been released (relating to financial year 2021).

What does this mean for your organisation?

Whichever way you look at it, sustainability reporting is here to stay and will continue to grow in importance. Already today, sustainability-related information informs and strengthens/complements financial information.

It furthermore has the ambition and potential to achieve a status comparable to that of financial information. And although sustainability information may currently be where financial information was about 100 years ago, it is safe to say that it will not take another century to achieve that equal footing.

So, what does this mean for your organisation?

Well, if you have not paid attention yet to ESG matters, it is high time you start doing this. For example, by developing the right indicators and by collecting the ESG-related data you already have. This will provide a first insight into your sustainability baseline and a first guidance on gaps to close.

As a next step, consider starting with an ESG or sustainability report as this will allow you to keep track of the information you gathered and to compare year after year.

And if your company is already engaged in some form of sustainability reporting, now is the moment to rethink and potentially expand the reporting process. Consider including the concept of double materiality (inside-out and outside-in). Look at the data you gather and the data you do not collect. Get inspired by the CSRD and EU Taxonomy.

In short, there is a lot of movement in the world of sustainability reporting. Don’t let your organisation be left behind.

Our team of experienced sustainability coaches can help you tackle sustainability reporting the right way. We guide you through the maze of requirements, assist you in structuring the data collection, and help determine the most useful governance for sustainability reporting in your organisation. Don’t hesitate to get in touch!

DISCLAIMER: In this article, neither Sustenuto nor any author provide tax, legal, accounting or investment advice. The material on this site has been prepared for general informational purposes only, does not claim to be comprehensive and does not and is not intended to provide, and should not be relied on for tax, legal, accounting or investment advice.

Every reasonable effort has been made to ensure the accuracy of the information provided in this blog. Nevertheless, it is possible that the information on our site includes errors or omissions. Sustenuto and any author do not accept any responsibility for loss which may arise from accessing or reliance on information contained in this site. Sustenuto and any author disclaim any liability for any errors or omissions. Articles and other publications on this site are current as of their date of publication and do not necessarily reflect the present situation.

Sources

This blog does not discuss the usefulness, relevance, adequacy, etc. (or not) of the reporting frameworks (or metrics therein) referred to above.

The NFRD also envisages other entities (such as credit institutions), which are not included in this blog.