As part of our commitment to guiding organisations through the complexities of sustainability reporting, Sustenuto is launching a new insight series on the revised European Sustainability Reporting Standards (ESRS). We begin with ESRS 1, which outlines the general requirements for preparing sustainability statements under the Corporate Sustainability Reporting Directive (CSRD).

Why ESRS 1 Matters

The European Financial Reporting Advisory Group (EFRAG) has responded to stakeholder feedback by streamlining ESRS 1 to reduce reporting burdens and improve clarity. This first revision introduces several key changes that impact how companies assess and disclose sustainability-related information.

Key Simplifications in ESRS 1

Double Materiality Assessment (DMA)

Companies now have two valid approaches:Bottom-up: Start from specific impacts, risks, and opportunities.

Top-down: Begin with your business model to identify relevant topics.

Both approaches aim for the same outcome, and quantitative scoring is no longer mandatory if a qualitative analysis sufficiently reflects material impacts.

Reduced Topic List

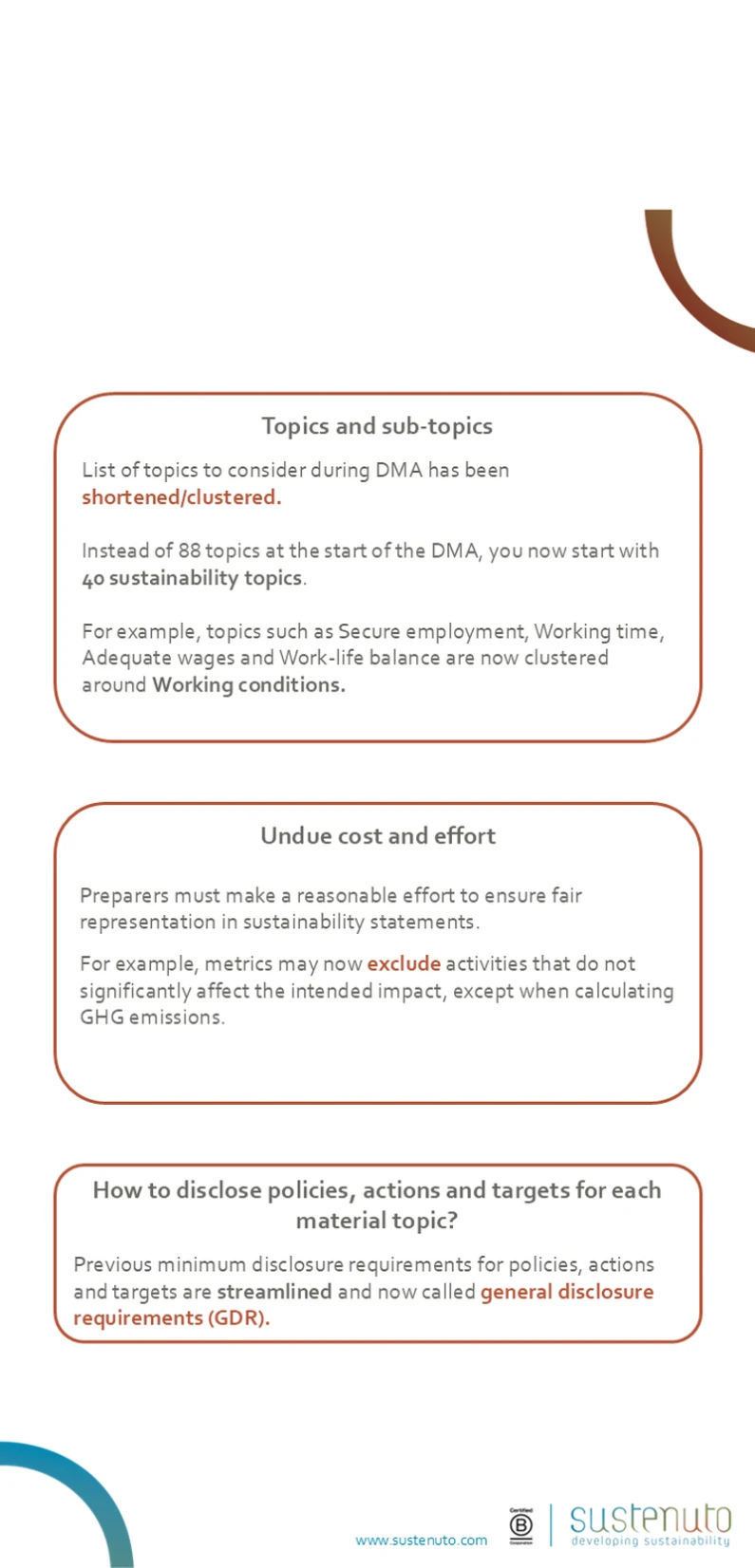

The number of sustainability topics has been cut from 88 to 40, with clustering for clarity. For example, “Secure employment,” “Working time,” and “Adequate wages” are now grouped under Working conditions.General Disclosure Requirements (GDR)

Minimum requirements for policies, actions, and targets have been streamlined into GDR, simplifying how organisations report on each material topic.Value Chain Boundaries

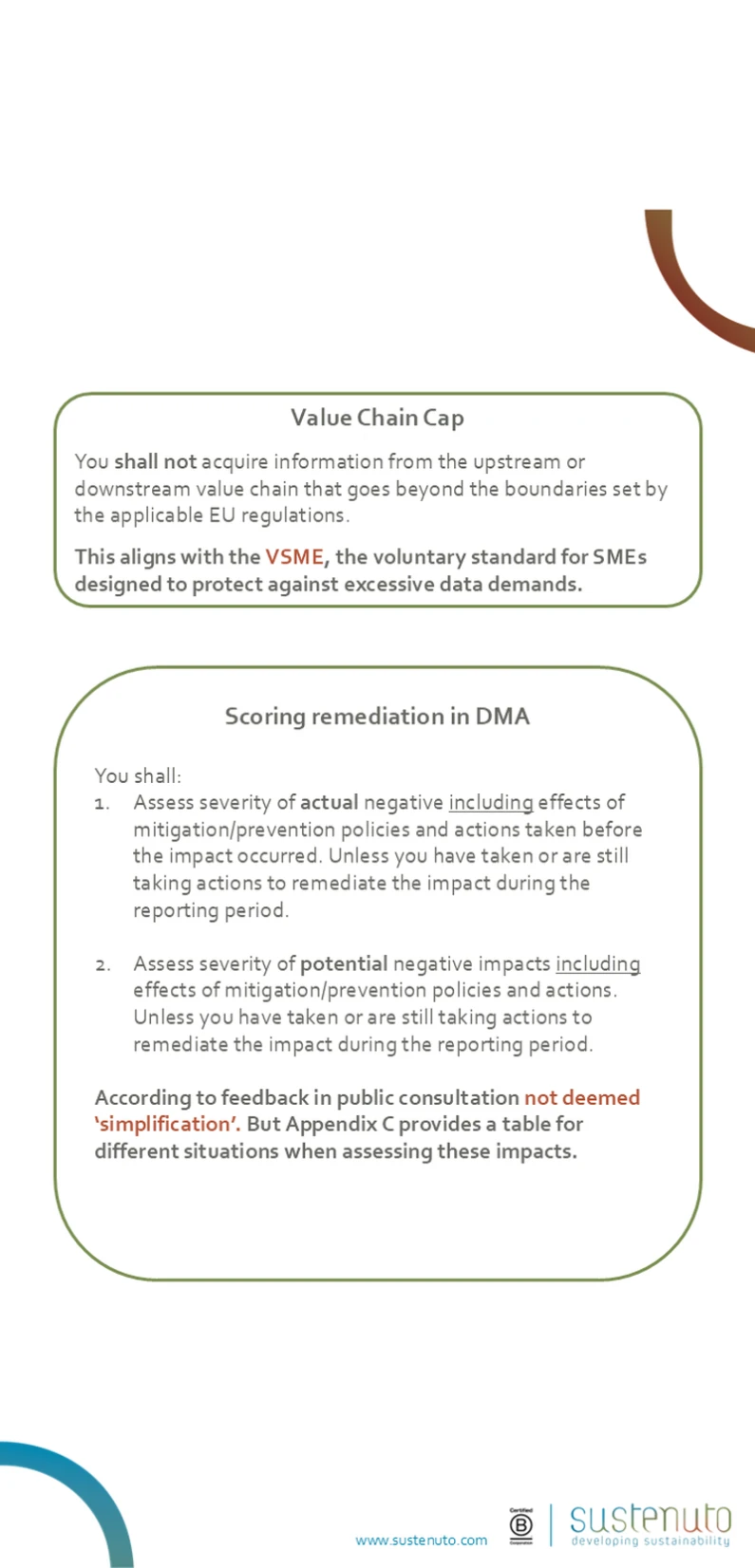

Companies are not required to collect data beyond EU-regulated boundaries. This aligns with the VSME voluntary standard for SMEs, protecting against excessive data demands.Voluntary Disclosures Moved to NMIG

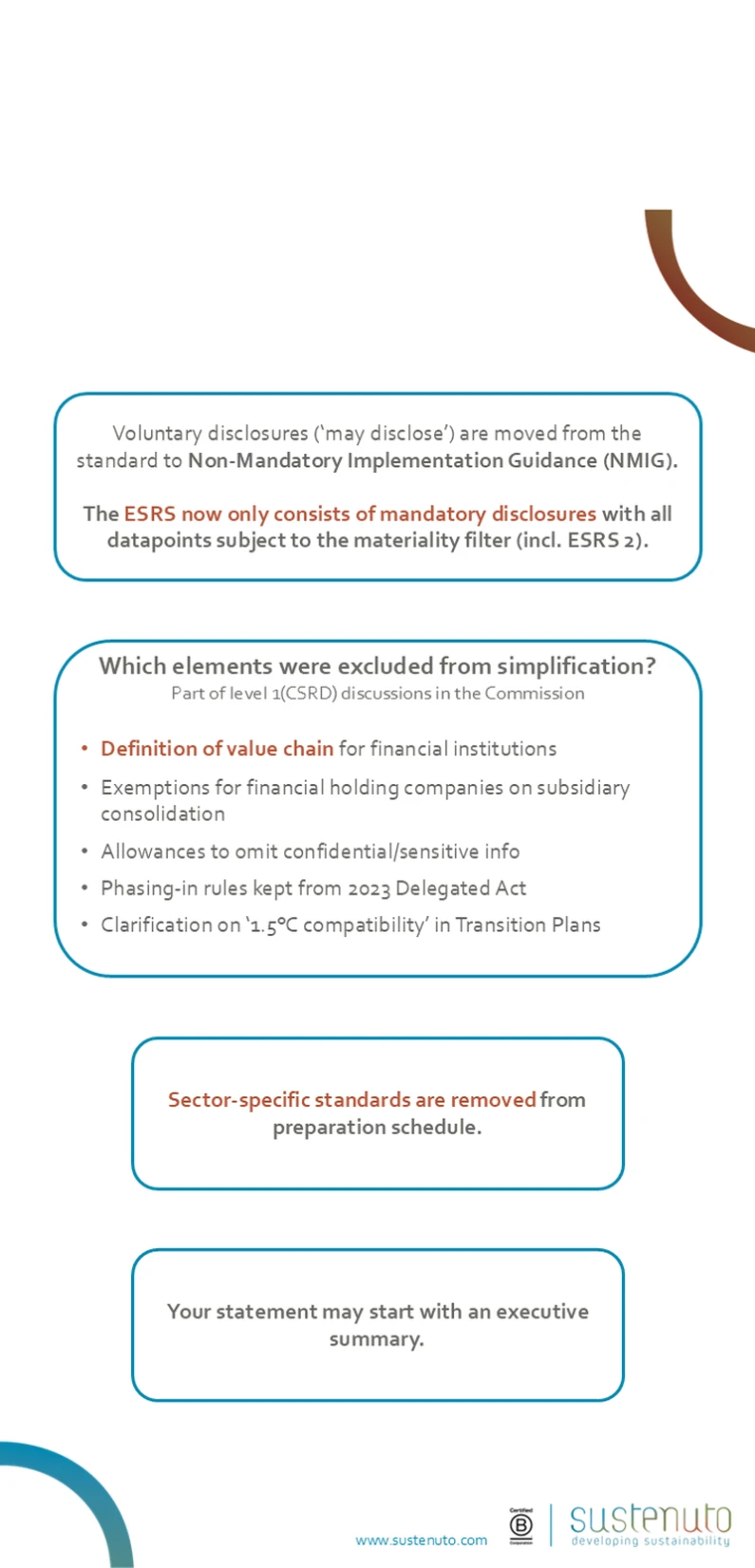

Non-mandatory disclosures are now part of the Non-Mandatory Implementation Guidance (NMIG), ensuring that ESRS only includes mandatory datapoints, all subject to the materiality filter.Sector-Specific Standards Removed

These are no longer part of the preparation schedule, allowing for a more unified reporting approach.Executive Summary Option

Sustainability statements may now begin with an executive summary, offering a concise overview of key disclosures.

What Was Not Simplified?

Certain elements remain unchanged due to ongoing CSRD-level discussions:

Definition of value chain for financial institutions

Exemptions for financial holding companies

Confidentiality allowances

Phasing-in rules from the 2023 Delegated Act

Clarification on 1.5°C compatibility in transition plans1

Public Consultation Open Until 29 September

Stakeholders still have time to provide feedback on the revised ESRS 1. If you're unsure how these changes affect your sustainability reporting or data management processes, our team at Sustenuto is here to help.

Learn more about ESRS 2 simplification here